French employees gained an average of eight days’ purchasing power in 2019

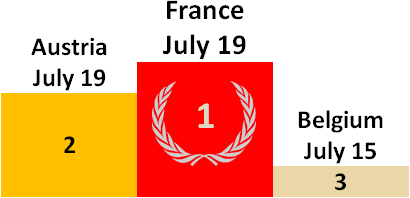

They worked until July 19 to finance public spending. The gap has narrowed substantially between France and the EU’s two other top taxers, Austria (July 19) and Belgium (July 15). The gap with the EU average (June 12) remains huge. But it is down to 37 days, compared to 45 days last year.

Paris, July 18, 2019 – Using data calculated by EY, the Institut économique Molinari is issuing its study, for the 10th consecutive year, on the true tax and social contribution pressure experienced by the average employee in the European Union (EU).

This study applies a solid methodology, uniform across the EU, with the specific aim of quantifying the tax and social contribution pressure actually confronting average wage earners in the current year. This brings out the true impact of the taxes and social contributions and how they are evolving.

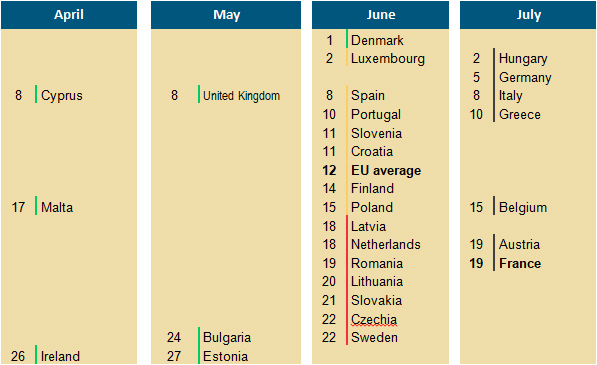

2019 TAX AND SOCIAL CONTRIBUTION FREEDOM DAYS FOR THE AVERAGE EMPLOYEE

WITHIN THE TOP TRIO, THE GAP BETWEEN FRANCE AND AUSTRIA HAS VANISHED

Just like last year, the three heaviest taxers of average employees are Belgium, Austria and France, but the gap has shrunk to the size of a pocket handkerchief.

Belgium is third on the podium, with tax and social contribution Freedom Day on July 15, two days later than in 2017. The former number one in this ranking (until 2015), then number two (in 2016 and 2017), became number three in 2018 and remains there in 2019, with 53.63% in tax and social contribution pressure on the average employee.

Austria remains in second place with tax and social contribution Freedom Day on July 19, one day later than last year. Year over year, tax and social contribution pressure has risen slightly, from 54.32% to 54.72%.

France remains the EU’s top taxer for the fourth year in a row. But tax and social contribution Freedom Day comes on July 19, eight days earlier than last year. This shift reflects the decline in tax and social contribution pressure, from 56.73% to 54.73%, with the application of decreases in social contributions by employers and employees promised during the 2017 presidential campaign.

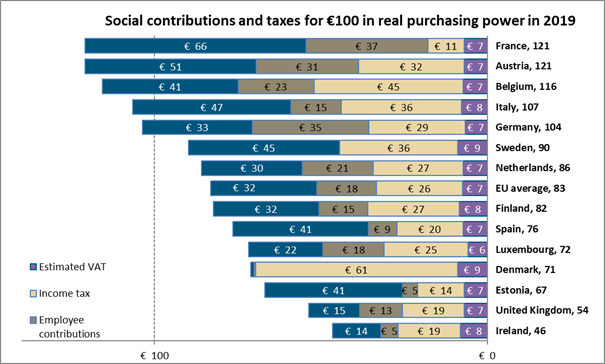

Before getting hold of €100 in real purchasing power, the average wage earner has to fork out €121 in social contributions and taxes in France, compared to €121 in Austria and €116 in Belgium. By way of comparison, the EU average is €83.

In six countries, more than half of work-related income is deducted in taxes and social contributions: France, Austria, Belgium, Greece, Italy and Germany. The average employee has no direct control over more than 50% of the fruits of her labour. Her influence over decision-making is, at best, indirect.

SOCIAL CONTRIBUTIONS FALL SIGNIFICANTLY AS CAMPAIGN PROMISES ARE IMPLEMENTED

For the second time since the launch of this indicator, the average French employee is recovering purchasing power. Tax and social contribution Freedom Day went from July 29, 2017, to July 27, 2018, a two-day gain. It now falls on July 19, an eight-day gain in one year and a 10-day gain in two years.

The weight of compulsory deductions taken from the average wage earner is declining very significantly in France. It now stands at 54.73% in 2019, compared to 56.73% in 2018 and 57.41% in 2017.

Employer contributions are down substantially. An employee with a gross salary of €38,582 comes fully within the scope of the conversion of the tax credit for competitiveness and employment (CICE) to lower contributions. In 2018, the CICE was 6% on salaries of less than two-and-a-half times the minimum wage. In 2019, this tax credit was converted to a six-point reduction in employer contributions for health coverage (7% instead of 13%). This measure amounts to a saving of €2,315 in employer contributions for the average French employee.

Employee contributions are also down significantly, in keeping with 2017 campaign promises. The average French employee is saving €1,215 in 2019 with the elimination of health and unemployment contributions. The elimination of health contributions (0.75%) amounts to a saving of €289, and the elimination of unemployment contributions (2.4%) provides a saving of €926 in 2019.

However, the 1.7% increase in the general social contribution (CSG) amounts to a loss of €663 in 2019. Similarly, the increase in the average employee’s tax base related to the decrease in social contributions leaves more taxable income, with €149 in additional income tax.

The gain in purchasing power for the average employee is €403. This is significant, but it is 19% below the €500 in additional purchasing power promised during the presidential campaign.

WAGE EARNERS IN FRANCE REMAIN THE MOST HEAVILY TAXED IN THE EU, WITH SOCIAL CONTRIBUTIONS GREATER THAN REAL PURCHASING POWER

The average French wage earner is, in theory, among the best paid in the EU, at €55 158 (ranking seventh), but is so heavily taxed (54.73% in social contributions and taxes on the full salary, highest in the EU) that there remains only €24,970 in real purchasing power (ranking 11th in the EU).

While employers face labour costs similar to those in the northern EU countries, the purchasing power of the average employee falls somewhere between that of the northern and southern countries.

Though paid more than a Swede or a Dane, the average French employee has 16% less purchasing power than the former and 30% less than the latter.

Social contributions alone (€25,737, highest in the EU) amount to more than real purchasing power (€24,970, ranking 11th). Social contributions come to 103% of real purchasing power. This is the EU record (average 53%).

HIGHER CONTRIBUTIONS AND TAXES DO NOT MEAN LIVING BETTER

The study shows that France’s tax and social contribution pressure is not synonymous with living better.

A crossing of data with the OECD publication How’s Life? shows that France, first in the EU in the real taxation rate of the average employee, is only 11th out of 21 EU countries in the latest OECD Better Life Index.

Quality of life seems better in various countries with lower tax and social contribution pressure. This is true of countries with a Bismarckian social tradition (Germany, Austria, Netherlands, Belgium), Beveridgean countries (United Kingdom, Ireland) and all the Nordic countries (Sweden, Finland, Demark).

TAX AND SOCIAL CONTRIBUTION PRESSURE LOWER ON AVERAGE IN THE EU

The average employee in the EU now faces a real taxation rate of 44.50%, stable compared to 2018.

Over the last year, nine EU countries have recorded a decline in levies on the average employee, while 17 have seen an increase.

The gap between the 19 eurozone countries and the nine countries outside the eurozone continues to widen. The euro zone benefited from more favourable taxation from 2010 to 2013, but the situation was reversed in 2014. Taxation in the euro zone stands at 44.72%, compared to 44.01% for the other EU countries in 2019.

QUOTATIONS

Cécile Philippe, president of the Institut économique Molinari and co-author

“Taxation on the average employee is down significantly in France, and this is excellent news.

“Since the launch of this IEM indicator, Tax and social contribution Freedom Day had kept going backwards, from July 26, 2010, to July 29, 2017. France had become the country that taxed average employees most heavily, without the indicators showing that the French got anything extra in terms of well-being.

“The situation moved in the opposite direction last year and this year. Average wage earners recovered 10 days of additional purchasing power. The reduction in social contributions implemented by the French government is headed the right way, even though the gap with the EU average remains very substantial.

“In the medium term, the issue for France continues to be an emphasis on reducing social contributions and taxes. This requires rethinking the scope of public action and, in contrast to fashionable ideas, breaking with the movement toward greater state control of social security. Experience shows that, when it comes to social security, centralisation is not a panacea, far from it.”

Nicolas Marques, Director at the Institut économique Molinari, co-author

“In the last few years, it has been too easy to forget the societal issue involved in reducing social contributions and taxes on wage earners.

“Over time, we have become number one in social contributions and taxes on average employees. The result is that growth is weaker in France than in the rest of the European Union. Unemployment remains abnormally high and is falling more slowly than anywhere else. Our fiscal deficits are not coming down significantly, and debt is taking off.

“The years 2018 and 2019 mark a break in this pattern, with the beginning of a reduction of taxation in France. Let’s hope this movement gathers strength in the years ahead.”

James Rogers, associate researcher at the Institut économique Molinari, co-author

“Despite the good news, French and Belgian wage earners are still devoting more than half of the amounts distributed by their employers in social contributions and taxes.

“It’s worth asking why they are not getting the top schools, the best health care and the most generous retirements in return and why they are not the leaders in indicators of human development or well-being.”

ABOUT THE AUTHORS AND THE METHOD

Tax and social contribution Freedom Day is the day when the average employee stops, in theory, paying social contributions and taxes and can use the fruit of her labour as she pleases.

This indicator measures the date starting on which the employee becomes free to apply the fruits of her labour in the way she wishes and not the date starting on which the employee may stop “working for society.”

The particularity of this indicator of economic freedom is that it puts the situation of average EU wage earners in tangible form by bringing together each country’s taxation of labour (social contributions and income tax) and of consumption (VAT). Calculations of employer and employee social contributions and of income taxes are done by EY for each of the 28 EU countries.

The study is written by Cécile Philippe, Nicolas Marques and James Rogers of the Institut économique Molinari (IEM).

The Institut économique Molinari (Paris and Brussels) is an independent research and education organisation. It seeks to stimulate the economic approach in the analysis of public policy, offering innovative alternative solutions that favour the prosperity of all individuals making up society.

THE STUDY IS AVAILABLE IN

• French at: https://www.institutmolinari.org/2019/07/18/la-pression-sociale-et-fiscale-reelle-du-salarie-moyen-au-sein-de-lue-en-2019/

• English at: https://www.institutmolinari.org/2019/07/18/the-tax-burden-of-typical-workers-in-the-eu-28/

FOR INFORMATION OR INTERVIEWS, CONTACT THE AUTHORS

• Cécile Philippe, President of the Institut économique Molinari

(Paris, French or English), cecile@institutmolinari.org, +33 6 78 86 98 58

• Nicolas Marques, Director at the Institut économique Molinari

(Paris, French), nicolas@institutmolinari.org, +33 6 64 94 80 61

• James Rogers, Associate Researcher at the Institut économique Molinari

(Brussels, English), james@institutmolinari.org, +32 497 946 840