Taxing e-cigarettes would be a mistake in the fight against smoking

Economic Note

Economic Note prepared by Frédéric Sautet, associate researcher at the Institut économique Molinari.

Read the Economic Note in PDF format

Read the Media release: Taxing electronic cigarettes would be a mistake in the fight against smoking

Following a series of volume decreases in sales of traditional cigarettes in France, down 3.4% in 2012, 7.6% in 2013, and 5.3% in 2014, sales appear to be stabilizing in 2015.(1) Even if this change in trend is confirmed (something far from certain), the decline in smoking in recent years has shown just how dependent governments (including France’s) have been on tax revenues from tobacco use. Giancarlo Scottà, a Member of the European Parliament, asked in 2013 what would replace tax revenues from tobacco. This parliamentarian’s concern was motivated entirely by the loss of tax revenue rather than by reasons of public health. Moreover, with this being a “tax hole” dug by electronic cigarettes (e-cigs), it would make sense to call upon e-cigs to help fill it, he said.

Other lawmakers see e-cigs as a nicotine product that should be taxed for reasons of symmetry: if tobacco is heavily taxed, then other nicotine-delivering items should be taxed likewise. Politicians of every stripe clearly wish to avoid being seen as encouraging nicotine consumption. However, according to many specialists, the potential benefits of e-cigs in the fight against smoking may be quite significant.

In the debate on e-cig taxation, public health considerations seem to be getting pushed aside, with a focus instead on tax revenues. But taxing e-cigs with the aim of offsetting tax losses from lower tobacco use could have impacts on public health. Hence the need to think clearly about how the tax tool could be used, taking both public health and tax revenues into account. In short, France may be at a turning point in tobacco consumption patterns, and any special taxation on e-cigs could compromise progress in the fight against smoking.

WHAT JUSTIFIES BEHAVIOURAL TAXATION?

There is nothing new about indirect contributions applied to certain substances (traditionally alcohol and tobacco) to control their use. But taxes that rely on principles of behavioural taxation are interfering increasingly with the lives of French people. Recently, drinks containing added sugar and sweeteners, as well as energy drinks, have ended up being taxed.

The arguments traditionally advanced to justify behavioural taxation rely on the notion of “externality”, meaning costs involuntarily borne by others. Smoking is a perfect case in point. Cigarette smoke may disturb people in the vicinity of a smoker, and they are not necessarily taken into account in the decision to smoke. A tax on cigarettes would lessen consumption and would lead smokers to act in a way that considers the externality they create by smoking. The same argument applies over time: smoking may cause health problems in the long term, at significant cost to taxpayers. The social cost of smoking (including matters such as lost productivity) may be higher than the private cost. Smokers would then tend to increase their tobacco use more than if they took these effects into account.(2)

Behavioural economics goes further. While traditional analysis assumes that individual choices are respectable (even though individuals may suffer later in life), behavioural economics regards individuals as insufficiently rational to take full account of tobacco’s harmful future impacts. Smokers would therefore put current consumption ahead of potential long-term risks. Smokers are generally aware of adverse effects in the future, but the more distant these effects are in time, the more they are disregarded.(3) Taxation in this instance is a mechanism that would boost self-control by helping cut consumption from the level it would be at if individuals were perfectly rational.(4) As such, the argument relying on externalities implies no moral judgment, whereas behavioural economics shows a degree of paternalism: it considers that smokers, left to themselves, would make a poor choice.

A more prosaic reason behind behavioural taxation involves the ever-rising social security deficit. Each year, the government needs to find ways to limit spending and boost revenues. It is sandwiched between higher social security contributions and spending cuts, equally tough options from a political standpoint. Increasing behavioural taxes in the name of public health is a far more acceptable approach. Rather than talk about “behavioural taxation”, experts have suggested using the notion of “public health contribution”,(5) which shows clearly that taxing tobacco is not fundamentally justified by behavioural change or externalities but rather by the financing of health care expenditures.

TOBACCO TAXES IN FRANCE

Behavioural taxation on traditional cigarettes has existed for many decades, with a sharp increase in the early 1990s under the Evin law. It could become a model for e-cigs, considering that most tobacco is consumed in the form of cigarettes in France.(6)

Despite efforts to simplify the taxation of cigarettes, this area remains complex and opaque. According to European directive 2011/64/EU1 currently in force, member states must adopt a hybrid tax structure for cigarettes. It combines a specific duty per product unit with an ad valorem duty (based on the average weighted retail price) augmented by a value added tax. The minimum excise duty rate (specific and ad valorem duties, not including VAT) comes to 60% of the averaged weighted retail price. The specific excise duty must fall between 7.5% and 76.5 % of the total taxes collected on the average weighted price. This amounts to a minimum overall excise duty of €90 per 1,000 cigarettes.(7)

Since January 1, 2011, the calculation of taxes on cigarettes relies on a “benchmark price” set annually by the government. For the year 2015, the decree of January 21, 2015, sets a benchmark price of €340 per 1,000 cigarettes in continental France, or €6.80 for a pack of 20 cigarettes.(8) Duties are calculated in proportion to the rates set out in the general tax code (Section 575A). The specific duty comes to €48.75 per 1,000 cigarettes, or €0.975 for a standard pack. The ad valorem portion amounts to 49.70% of the price. For 1,000 cigarettes sold at €340, the consumption tax that is borne is €48.75 + €168,98 = €217,73, or €4.35 per pack of 20 cigarettes (64% of the selling price). The VAT accounts for 16.67% of the selling price, or €1.13.(9) The portion of taxes in the selling price of a pack of cigarettes comes to €5.48, or 80.63%. The rest is shared between the retailer and the manufacturer (about 8% and 12% respectively of the total price).(10)

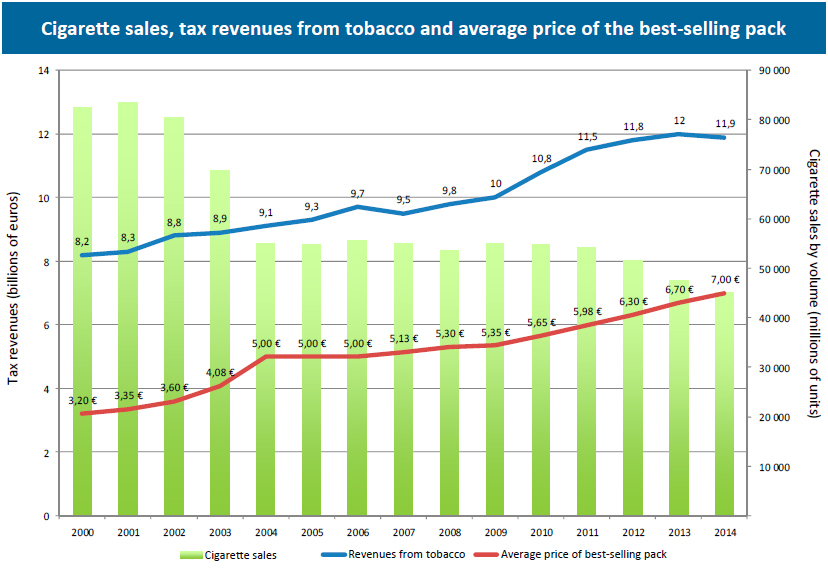

Cigarette sales rose in volume until the early 1990s. Whereas the relative price of tobacco had remained fairly stable between 1975 and 1990, it increased early in that decade because of the Evin law, which brought sales growth to a halt through substantial increases in excise duties and of the average selling price of a pack of cigarettes.(11) The decline in purchases by volume that became more pronounced between 2001 and 2004 (-34%) and again between 2011 and 2014 (-17%) was caused partly by a sharp boost in the price of tobacco (+49% between 2003 and 2004 and +17% between 2011 and 2014) and also by growth in illicit markets and the advent of e-cigs. Since 2000, tax revenue from tobacco has continued to rise, with consumption falling in volume though not in value, except in 2007 and in 2014, when there was a slight shift. We may be nearing a point where higher excise rates will no longer be enough to offset the decline in sales by volume.(12)

SHOULD E-CIGS BE TAXED LIKE TRADITIONAL CIGARETTES?

Some people regard e-cigs as a complete alternative to traditional cigarettes. Logic would suggest some similarity between tobacco and other products containing nicotine, implying that both should be taxed the same way. We could even apply the principle of fair taxation, according to which identical products or activities cannot be taxed differently.

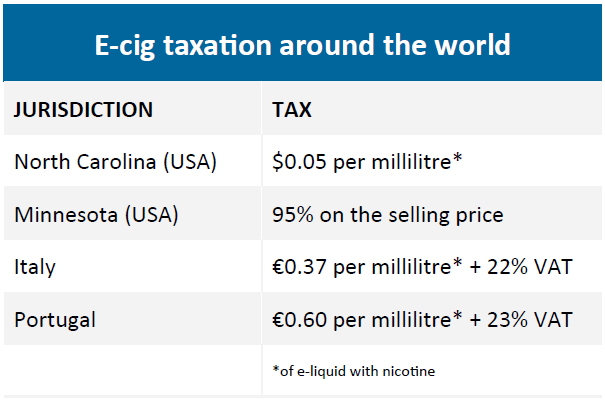

For the moment, however, there exist only a handful of jurisdictions that tax e-cigs: two U.S. states(13) as well as Italy and Portugal. These special taxes apply in particular to the nicotine-containing e-liquid. The European Union (EU) has thought of taxing e-cigs but has not yet reached a decision.(14) The French government had considered introducing a tax on e-cigs in its 2014 budget, but the idea was deemed inconsistent with the promise at the time of a “tax pause”. There are several ways of taxing e-cigs. The most obvious one consists of imposing a tax per millilitre of nicotine-containing e-liquid, but other approaches may also be envisaged. This tax may also be based on the concentration of nicotine in e-liquids. In the Italian case, a complex formula estimates the number of puffs obtained from a millilitre of e-liquid to standardize this form of taxation with that on cigarettes.

The issue of taxing e-cigs can set the mind fuming. E-cig supporter Jean-François Etter suggests in his book La vérité sur la cigarette électronique (The truth on electronic cigarettes) the imposition of a tax that would help finance studies on their impact. Professor Philippe Presles holds the same view.(15) Yves Martinet, president of the Comité national contre le tabagisme (National committee against smoking), urges the taxation of e-cigs as an intermediate product between tobacco and everyday consumer products subject only to the VAT.(16) The result is that e-cig defence groups are on the alert. Sébastien Bouniol, vice-president of the Association indépendante des utilisateurs de cigarette électronique (Independent association of electronic cigarette users), is firmly opposed to any idea of taxing e-cigs.(17) The same is true of Mickael Hammoudi, president of the Collectif des acteurs de la cigarette électronique (Electronic cigarette collective).

Indeed, while they may provide an experience similar to that of tobacco, e-cigs do not have the same chemical properties. Although they may be an addictive product, they are likely to produce much less harmful effects on the human body.(18) “The risk from prolonged nicotine intake is not nearly as great [with e-cigs] as continuing to smoke.”(19) E-cigs provide nicotine without tobacco combustion products (tars and carbon monoxide). Moreover, considering that e-cigs are a better way of quitting smoking than current nicotine-containing substitutes, they should, in contrast, benefit from favourable tax treatment so that they can contribute fully to the fight against smoking in France.(20) This would imply, however, treating e-cigs as a drug available only in pharmacies, limiting the market and its development.(21)

There remains the argument of externalities and passive inhalation, one of the most commonly used theoretical reasons for taxing tobacco. The issue is whether the aerosol emitted by e-cigs contains hazardous substances. With tobacco smoke, pollution is mostly particulate; with e-cigs, it is mainly gaseous. According to the Dautzenberg Report, the risks from the droplets contained in e-cig aerosol are theoretically more than 100 times lower than from exposure to tobacco smoke.(22) But some works indicate that passive vaping (a term applied to e-cig use) is not necessarily free of danger: after exposure to e-cigs, levels of serous cotinine (a nicotine metabolite) have been found that are almost identical to those of cigarettes.(23) However, the Dautzenberg Report says the quantity of known carcinogens in e-cig aerosol is far lower than in cigarette smoke (formaldehyde concentration levels are five to ten times lower),(24) although some studies state that the formaldehyde level is higher than that of cigarettes.(25) In general, e-cigs would appear to reduce significantly the problems of externality that go with smoking. And prohibiting vaping in public places (especially in workplaces) should limit, if necessary, the problem of passive vaping.(26)

These considerations would tend to prove the futility of taxing e-cigs. In brief, the basic argument against taxing e-cigs relies both on its relative harmlessness and its role as an alternative to tobacco. A number of specialists echo this. Professor Dautzenberg frequently reaffirms the less hazardous nature of e-cigs compared to traditional cigarettes.(27) Dr John Britton of the Royal College of Physicians in England says the same thing. Comparing the hazards of cigarettes with those of e-cigs, he gives scores of 100 (very dangerous) to the former and 5 to the latter. If every smoker in the United Kingdom went over to e-cigs, he explains, five million human lives would be saved. Even France’s Social Security evaluation and monitoring mission, led by rapporteurs Catherine Deroche and Yves Daudigny, does not call for an additional tax on e-cigs but only for controls on product quality: “This amounts to taxing products that are likely to be substituted for those of which the consumption is harmful or inadvisable in too great a quantity… It will undoubtedly raise the inappropriate nature of taxing electronic cigarettes insofar as they appear to constitute a less toxic substitute for traditional tobacco products.”(28)

The intermediate taxation proposal from Yves Martinet would have the effect of reducing e-cig consumption. With the health impact of e-cigs on vapers (active and passive) far lower over time than what is caused by traditional cigarettes, it would be extremely difficult to justify any taxation beyond the VAT. Arguments justifying behavioural taxation of traditional cigarettes are harder to defend in the case of e-cigs. Two considerations merit attention. First, taxation would promote the growth of illicit trade in e-cigs and especially of e-liquids, with all the problems this would entail with respect to their quality. Second, it could introduce a taxation dynamics of the sort observed with tobacco. The temptation to bring in an e-cig tax in the 2014 French budget will re-emerge in the future if the e-cig market continues to grow and tax revenues from tobacco continue to decline.(29) One tax increase will lead to another. Once the door is opened to taxation, it will not be limited in its growth. Yves Martinet’s position is therefore untenable in the long term.

Finally, the role of lobbying in tax creation is not to be neglected. North Carolina is one of two U.S. states to tax e-cigs. It also has an economy traditionally oriented to tobacco production. Cigarette maker R. J. Reynolds, headquartered in Winston-Salem in this same state, worked to establish the five-cent tax per millilitre of e-liquid.(30) R. J. Reynolds also wants an excise tax on e-cigs to be applied across the United States.(31) The company also lobbied to prohibit e-cig access to minors in North Carolina. This was approved in a 2014 vote. Whether or not the prohibition is considered justified, the fact remains that, by limiting the chance for young people to vape, American tobacco producers continue to prop up their traditional market.(32)

CONCLUSION: TAXING E-CIGS WOULD BE AN ERROR IN THE FIGHT AGAINST SMOKING

According to professionals in the field, e-cig taxation is almost a fait accompli. “We are expecting to see higher taxes in one or two years and have even budgeted for it in our three-year forecast,” says Karin Warin, founder of the Clopinette brand, the French leader in electronic cigarette distribution. She adds: “The tobacco market amounts to €14 billion, compared to €200 million for electronic cigarettes. Clearly, raising our taxes will not offset the losses in tax revenues from tobacco products.”(33)

However, e-cig use and distribution is now regulated. Most restrictions on traditional cigarettes now apply to e-cigs. The difference lies in taxation. The presence of nicotine in some e-liquids may pose a problem. But political courage lies in acknowledging and affirming the essential role that e-cigs could play in the fight against smoking, as the British government is proposing to do. By keeping e-cigs among the everyday consumer products subject only to the VAT, the French public authorities would show their goodwill and their long-term vision.

About the author

Frédéric Sautet holds a doctorate in economics from the Université de Paris Dauphine and did his post-doc at New York University. He has been an economic advisor at the New Zealand Treasury and a senior economist at the Commerce Commission (New Zealand competition watchdog). He taught economics at the Université de Paris Dauphine, New York University and George Mason University. He now teaches at The Catholic University of America. He started collaborating with IEM in 2014.

References

1. See “Les ventes de cigarettes se stabilisent”, Le Figaro, April 9, 2015.

2. Net social cost needs to take account of premature deaths among smokers, reducing health care spending substantially. See Suranovic, R. Goldfarb, T. Leonard, “An economic theory of cigarette addiction”, Journal of Health Economics, 1999, Vol. 18, 1-29. p. 22. See also J. Gooris, O. Sautel, “13 euros, c’est le prix du paquet de cigarettes ‘socialement responsable’!”, Microeconomix, March 19, 2015.

3. Theorists call this “hyperbolic discounting”.

4. Behavioural economics also affirms, contrary to some criticism, that poor people benefit from taxation because they potentially make the worst judgments. Each smoker would have his or her own tax level that helps improve self-control. Responses to taxation vary by age, social class and country. But this approach generally justifies high taxes.

5. See Y. Daudigny and C. Deroche, Report on behavioural taxation (recommendation no. 1), Mission on behavioural taxation, French Senate, 2014.

6. The figure is around 80% of tobacco consumed in the firm of cigarettes. See E. Janssen and A. Lermenier-Jeannet, “Tableau de bord mensuel des indicateurs du tabac : bilan de l’année 2014”, Observatoire français des drogues et des toxicomanies, March 9, p. 2.

7. See the excise duties applicable to cigarettes (http://ec.europa.eu/taxation_customs/taxation/excise_duties/tobacco_products/cigarettes/index_en.htm) and also the Daudigny Deroche Report, p. 68.

8. For details of the decree on January 21, 2015, see: http://www.legifrance.gouv.fr/affichTexte.do?cidTexte=JORFTEXT000030160575&dateTexte=20150714

9. The VAT rate as of January 1, 2015 is 20%, but the VAT accounts for 16.67% of the selling price, which is the so-called “inclusive” rate.

10. See the Circular of April 23, 2015, on applicable taxation of manufactured tobacco products from the French ministry of finance and public accounts

(http://circulaires.legifrance.gouv.fr/pdf/2015/04/cir_39509.pdf)

11. See D. Besson “Consommation de tabac : la baisse s’est accentuée depuis 2003”, December 2006, National Institute of Statistics and Economic Studies.

12. Determining which way tax revenues are headed can be tricky, because the advent of new substitutes (e-cigs and illicit markets) changes the price elasticity of demand. This makes it hard to anticipate whether a new rise in excise duties could offset a possible decline in sales, But looking at an average price of €6.80 for a pack of cigarettes, we see that taxes account for €5.48. Let us assume that, in 2014, about 500,000 smokers quit and went over to e-cigs or turned to the black market. This would represent a decline in tax revenues of about €2.74 million per week if these people smoked a pack a week. In the course of a year, this would represent a shortfall of more than €142 million, roughly equal to the decline recorded in 2014. For an analysis of the impacts, see J.-M. Binetruy, J.-L. Dumont and T. Lazaro, “Rapport d’Information sur les conséquences fiscales des ventes illicites de tabac”, French National Assembly, October 2011.

13. North Carolina (5 cents per millilitre of nicotine-containing e-liquid) and Minnesota (95% on the selling price). However, 21 states and the District of Columbia have attempted in 2015 to introduce new taxes on e-cigs. This attempt failed in the following eight states: Arizona ($0.18), Arkansas ($0.075), Indiana (24%), Kentucky (40%), Montana ($0.0173), Nevada (30%), New Mexico ($0.04) and Virginia ($0.40 and $0.18). In other states, laws are under discussion: Alabama ($0.25), Hawaii (80%), Maine ($2 fixed rate), Massachusetts ($3.51 fixed rate), New Hampshire (73.94%), New Jersey (75%), New York (75%), Ohio (60%), Oregon (81.25%), Rhode Island (80%), Utah (no rate specified in the legislation), Vermont (46%), Washington State (95%) and Washington, D.C. (70%).

14. See “European Commission considers taxing ecigarettes, Financial Times, Feb. 18, 2015.

15. See “Une taxe sur la cigarette électronique oui mais pour quoi faire?” Presles is the author of the book La cigarette électronique – Enfin la méthode pour arrêter de fumer facilement (Editions Versilio).

16. According to Yves Martinet, “intermediate taxation should be applied on e-cigarettes, taking account of the risk to users’ health. This tax should be higher than what applies to everyday products but not as high as the tobacco tax.” See “La cigarette électronique échappera-t-elle longtemps aux taxes”, 20 Minutes, Jan. 13, 2014.

17. According to Sébastien Bouniol, “Italy is a good example, because electronic cigarettes were doing quite well before this 73% tax was applied on the overall price. Sales of electronic cigarettes then fell: this had an immediate effect on the destiny of electronic cigarettes, and people either continued using electronic cigarettes through black market channels or returned to tobacco.” See “Quelle taxation pour la cigarette électronique”, La cigarette électronique : quel avenir pour cet objet controversé ?

(http://controverses.ensmp.fr/public/promo13/promo13_G3/www.controverses-minesparistech-1.fr/_groupe3/indexe158.html?page_id=311).

18. See F. Sautet, “Smoking or vaping: the revolution in tobacco and nicotine consumption”, Institut économique Molinari, March 2015.

19. See B. Dautzenberg, “Rapport et avis d’experts sur l’e-cigarette“, Office français de prévention de tabagisme, May 2013, p. 90.

20. E-cigs work better than traditional methods for taking care of smoking, sales of which have been falling since 2010. Not even nicotine inhalers provide the same satisfaction as e-cigs. Inhalers take 25 minutes to cause relief for the lack of nicotine. The time is much shorter for e-cigs, which also have the advantage of producing fewer side effects than inhalers. It is also a matter of the ability to reproduce the sensation on a vaper’s throat at the time of inhaling. A growing number of scientific articles show a significant effect of e-cigs in smoking cessation. See F. Sautet, “Smoking or vaping”, p. 2.

21. This course is unlikely, however, given regulatory shifts within the EU.

22. Dautzenberg Report, p. 95. “Even in the most extreme conditions, it is not possible to reach levels deemed toxic in a room where e-cigs are used.” Dautzenberg Report, p. 96.

23. Dautzenberg Report, p. 98.

24. Dautzenberg Report , pp. 78 and 97.

25. The Japanese study indicating high levels of formaldehyde did not reproduce normal vaping conditions. See F. Sautet, “Fumer ou vapoter”.

26. Members of the French National Assembly’s social affairs committee adopted an amendment on March 18, 2015, prohibiting vaping in certain public places.

27. See “Cigarette électronique : un succès justifié contre le tabac”, Le Figaro, Jan. 30, 2015.

28. Daudigny Deroche Report, p. 115. Supporters of taxation often neglect to mention that vaping is far less harmful than burning tobacco. See, for example, “E-cigarette taxation: Frequently asked questions”, a document issued by the Tobacco Control Legal Consortium in March 2015, which makes no mention of the advantages of e-cigs compared to tobacco.

29. This could be the case with the introduction of neutral packaging. According to a recent study by economic consulting firm MAPP, introducing such packaging could lead to a drop in annual tax revenues in France of between €413 million and €3.4 billion. See “Paquet neutre : deux milliards d’euros de recettes fiscales en moins ?”, La Tribune, July 22, 2015.

30. See “Taxing E-Cigarettes in Tobacco Country”, E-Cigarette Tax Policy Research, January 2015. Italy is in a similar situation, with some commentators saying the new legislation favours the traditional tobacco industry, especially Philip Morris. See “Italian e-cigarette firms say new tax benefits tobacco”, Reuters Health, February 2015.

31. See “Reynolds American suggests state tax rate for e-cigarettes”, Winston-Salem Journal, May 13, 2014.

32. It is worth noting that most U.S. states have passed laws prohibiting e-cig sales to minors.

33. See “Quelle taxation pour la cigarette électronique?”