The numbers show that the GAFA Four are already paying taxes at normal levels. Economic analysis shows they will be collecting a tax that will hit our consumers and producers.

Media release

Paris, March 12, 2019 : The Institut économique Molinari is issuing an original study on the earnings and taxation of Google, Apple, Facebook and Amazon, including comparisons with the top European big-cap companies that form the Euro Stoxx 50 and Stoxx Europe 50 indices.

THIS STUDY SHOWS THAT :

- The orders of magnitude cited by the French authorities are unsubstantiated. The U.S. digital majors are not paying 14 points less in taxes than French or European companies.

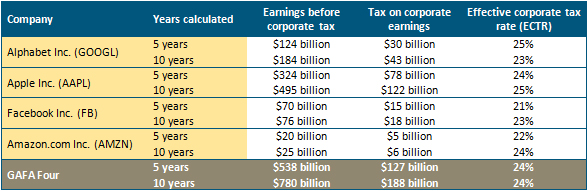

- Factual analysis of earnings shows that the GAFA Four paid 24% in taxes on their global profits in the last five years and in the last 10 years.

- This level of taxation, far from being abnormally low, is slightly higher than average taxation in the OECD countries.

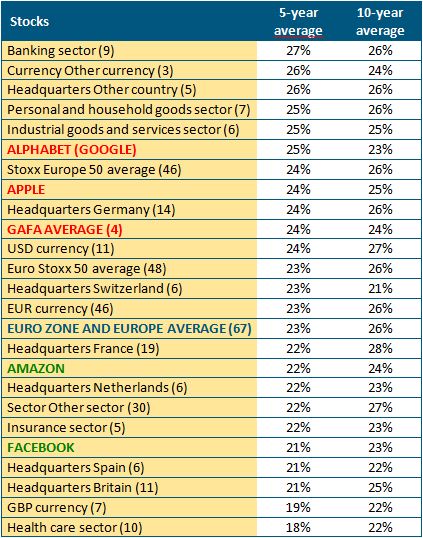

- The GAFA pay taxes similar in magnitude to the big euro zone and European companies that form the Euro Stoxx 50 and Stoxx Europe 50 indices. In the last five years, they paid one point more in taxes. In the last 10 years, they paid two points less.

Tax comparison of the GAFA and the main euro zone or European companies

Data from the last five and last 10 annual earnings reports. Average effective corporate tax rate (ECTR) on earnings calculated by the IEM (details appended). Figures exclude BP, Essilor, Glencore, Nokia and Vodafone.

- France’s digital services tax (TSN, or taxe sur les services numériques) is not a public finance issue, with an expected gain amounting to just 0.03% of government revenues.

- It poses a daunting threat to low-margin companies. If a 3% tax were applied on the global business of the large euro zone or European companies, 20% of them would see their pre-tax earnings slashed by 50% or more. Amazon would be especially hard hit upon initial analysis, with an average global margin of 2.6% over the last 10 years.

- According to the tax incidence theory, the big U.S. players, with the lead they have built, should be able to shift the TSN onto other players, consumers or business partners.

- Beyond consumers, the TSN would penalise European digital players(Blablacar, Criteo, Le bon coin, Se loger, Spotify, SoLocal, etc). With their lesser weight, they are less able to shift the effect of the tax onto other players. The TSN would contribute to greater concentration and higher dependency on foreign companies in a fast-growing field.

- The TSN also carries risks for traditional European players that need to make a digital shift to maintain direct contact with their customers. Sooner or later, it is likely to affect these European companies by limiting their ability to catch up to pure players that have taken a significant lead.

OTHER TAX LESSONS

The European Commission emphasizes theoretical models based on existing tax provisions (PwC and ZEU, 2017). In contrast to the official French line, these simulations show that :

- Most of the tax distortions between digital players result from national measures, thereby establishing differences in treatment between European countries. Several states, including France, have set out to be more lenient toward companies that consume research, development and innovation while taxing other companies more heavily.

- France is the worst country in which to locate a business that does not require research, development and innovation. With a 38% tax compared to an EU average of 21%, it ranked last among the 28 EU countries.

The TSN adds a new production tax, augmenting a flaw in the French system. Total production taxes already amount to as much in France as in 23 EU countries combined, including Germany. In relative terms, these production taxes were twice as high as the EU average and six times as high as in Germany (shown under Other taxes, aggregate D.29).

RESOURCES

The study is available (in French) on our website.

A set of European charts (Datawrapper) is provided : https://datawrapper.dwcdn.net/jVM47/3/

Effective tax rates on GAFA earnings (5 years and 10 years)

Data from results ending Dec. 31, 2018 for Alphabet, Facebook and Amazon. Sep. 29, 2018 for Apple. ECTR calculated by the IEM. Details appended.

Change in effective corporate tax rates for the GAFA Four and 67 euro zone and European stocks over 10 years and 5 years

Data from earnings reports. Effective corporate tax rate (ECTR) on earnings calculated by the IEM. Details of data appended. Figures in parentheses specify the number of stocks used to calculate the average. Figures exclude BP, Essilor, Glencore, Nokia and Vodafone.

QUOTES

Nicolas Marques, Managing Director of the Institut économique Molinari (IEM) and author of the study :

“The digital tax is misrepresented as a social justice measure. It is supposed to correct a discrepancy in taxation between Europe and the United States, which is non-existent. It will hit back at consumers and European companies, with experience showing that players in a position of strength have the ability to shift the tax onto others. “The digital tax illustrates flaws in the French tax system. Two years of work on a tax matter amounting to barely 0.03% of government revenues, in a badly put-together project with imprecise orders of magnitude and no serious impact study. Above all, a new production tax that will penalise consumers and hold back the acclimatisation of our economies to the digital world, the black gold of a modern economy.”

Cécile Philippe, President of the Institut économique Molinari (IEM) :

« Unlike the concerted approach taken by the OECD, the French digital tax is likely above all to penalise the French and European economy and consumers. « This tax is likely to weaken digital competition and add to concentration. The digital majors will easily be able to shift the costs to other sectors, confining themselves to the role of tax collectors. Meanwhile, this new tax brings a specific risk to bear on European digital companies that have fallen behind and are less able to shift the costs onto the rest of the economy. « It also risks debilitating our traditional companies that need to invest in digital to make their transition.”

FOR INFORMATION OR INTERVIEWS, CONTACT :

Nicolas Marques, Managing Director, Institut économique Molinari

(Paris, in French)

nicolas@institutmolinari.org

+ 33 6 64 94 80 61

Or Cécile Philippe, Presidente, Institut économique Molinari

(Paris, Brussels, in French or English)

cecile@institutmolinari.org

+33 6 78 86 98 58

ABOUT THE IEM

The Institut économique Molinari (IEM) is a research and education organisation with the mission of promoting individual freedom and responsibility. The Institute aims to facilitate change by spurring debate around preconceived ideas that engender the status quo. It seeks to stimulate the emergence of new consensus positions by offering an economic analysis of public policy, demonstrating the value of dialogue and indicating the benefits of more lenient regulation and taxation. The IEM is a non-profit organisation financed by voluntary contributions from its members : individuals, foundations and businesses. Putting intellectual independence foremost, it accepts no public subsidies.